ASK A FINANCIAL PLANNER

Wills and trusts are common documents used in estate planning. While each can help in the distribution of assets at death, there are important differences between the two.

What is a Will?

A last will and testament is a legal document that lets you direct how your property will be dispersed (among other things) when you die. It becomes effective only after your death. It also allows you to name a personal representative (executor) as the legal representative who will carry out your wishes.

What is a Trust?

A trust is a legal relationship in which you, the grantor or trustor, set up a trust, which holds property managed by a trustee for the benefit of another, the beneficiary. A revocable living trust is the type of trust used most often as part of a basic estate plan. “Revocable” means you can make changes to the trust or even revoke it at any time.

A living trust is created while you’re living and takes effect immediately. You may transfer title or ownership of assets, such as a house, boat, automobile, jewelry, or investments, to the trust. You can add assets to the trust and remove assets thereafter.

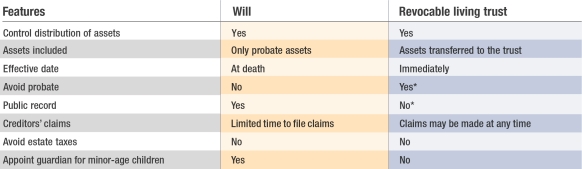

How Do They Compare?

While both a will and a revocable living trust enable you to direct the distribution of your assets and property to your beneficiaries at your death, there are several differences between these documents. Here are some important ones:

1. A will generally requires probate, which is a public process that may be time-consuming and expensive. A trust may avoid the probate process.

2. A will can only control the disposition of assets that you own at your death, including property you held as tenancy in common. Even if you have a revocable living trust, you should have a will to control assets not captured in the trust. It cannot govern the distribution of assets that pass directly to a beneficiary by contract (such as life insurance, annuities, and employer retirement plans) or by law (such as property held in joint tenancy).

3. Your revocable trust can only control the distribution of assets held by the trust. This means you must transfer assets to your revocable trust while you’re living, which may be a costly, complicated, and tedious process.

4. Unlike a will, a trust may be used to manage your financial affairs if you become incapacitated.

5. If you own real estate or hold property in more than one state, your will would have to be filed for probate in each state where you own property or assets. Generally, this is not necessary with a revocable living trust.

6. A trust can be used to manage and administer assets you leave to minor children or dependents after your death.

7. In a will, you can name a guardian for minor children or dependents, which you cannot do with a trust.

Generally, most estate plans that use a revocable trust also include a will to handle the distribution of assets not included in the trust and to name a guardian for minor children. In any case, there are costs and expenses associated with the creation and ongoing maintenance of these documents. Keep in mind that wills and trusts are legal documents generally governed by state law, which may differ from one state to the next. You should consider the counsel of an experienced estate planning professional and your legal and tax advisers before implementing a trust strategy.

SESLOC members have access to our knowledgeable CFS* Financial Advisor, offered through SESLOC Wealth Management »

Prepared by Broadridge Investor Communication Solutions, Copyright 2020.

SESLOC Wealth Management is provided through our relationship with CUSO Financial Services, L.P. (CFS)* an Independent Broker-Dealer and SEC Registered Advisor formed for the express purpose of serving Credit Union member’ investment and financial planning needs.

*Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA/SIPC) and SEC Registered Investment Advisor. Products offered through CFS adre not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including potential loss of principal. Investment Representatives are registered through CFS. SESLOC has contracted with CFS to make non-deposit investment products and services available to credit union members. CFS and its representatives do not provide tax advice. For specific tax advice, please consult a qualified tax professional.